What Should You Include on Your Chart of Accounts?

Your chart of accounts (COA) is a list of account numbers and names that are relevant to your small business. It helps keep your financial information organized and is the first step of establishing your accounting system. Your COA enables you make more informed financial decisions by showing you a clear picture of where you’re earning money and how you’re spending it.

Setting up your COA is not as complicated or daunting as it may sound. For each account, assign a number and a name that makes sense to you and your accountant. You’ll use those accounts when recording transactions in your general ledger.

A chart of accounts is typically broken into five categories.

1. Assets

Your asset accounts track what your company owns, including cash and inventory. Usually, asset accounts are assigned numbers that start with 1000. For example, your cash account may be 1000, and accounts receivable may be 1010.

The first accounts listed in your assets category should be current assets, which are assets that can be converted to cash quickly. Current assets include:

- cash

- short-term investments

- accounts receivable

- inventory

After you’ve assigned numbers to your current assets, assign numbers to your fixed assets. Fixed assets are purchased for long-term use and are not easily converted into cash. Fixed assets include:

- land

- buildings

- vehicles

2. Liabilities

Your liability accounts keep track of anything your company owes, including debt obligations. Typically, liability account numbers range from 2000-2999.

Start your list with current liabilities, which are debts due within one year. Current liabilities include:

- accounts payable

- payroll tax liability

- sales tax liability

- credit cards

After you’ve added your current liabilities, move on to your long-term liabilities, which are not due within the next 12 months. Long-term liabilities include:

- mortgage

- long-term loans

- deferred income taxes

3. Owner’s Equity

Owner’s equity accounts track your investment in your small business. These accounts typically start at 3000. You may also have an account for retained earnings, which is the net income your business has after paying out dividends to shareholders and is typically invested back into the company.

4. Revenue

Revenue accounts help you track your company’s sources of income and are typically numbered in the 4000-range. Revenue accounts include:

- sales

- returns and allowances

- income from interest

- costs of goods sold

5. Expenses

Expenses track what your small business pays. Expense accounts typically start at 5000. Some of your expense accounts will be related to your liability accounts, so you can track how much of your debt you’ve paid off. Expense accounts include:

- marketing and advertising

- contract labor

- office supplies

- travel and meals

- salaries and wages

- payroll taxes

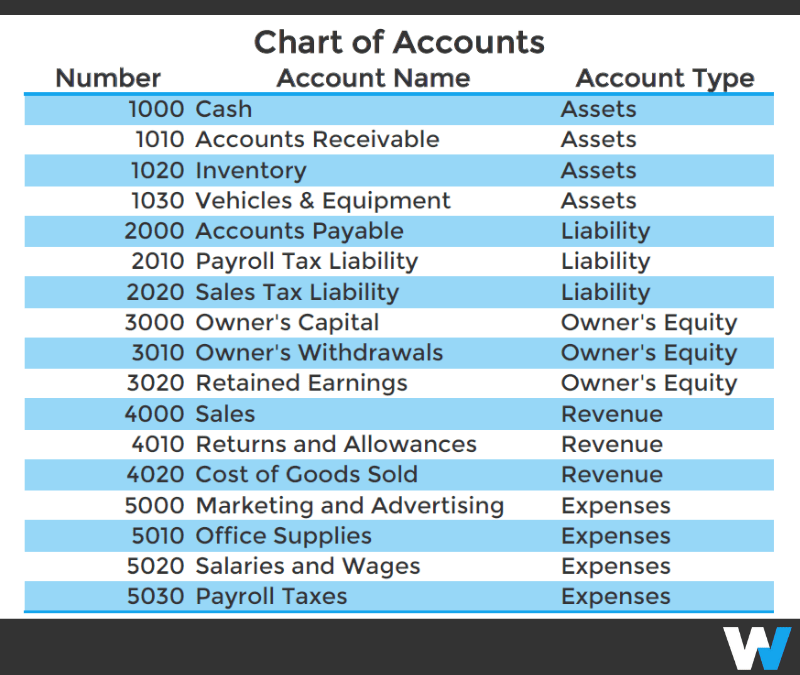

Sample Chart of Accounts

After you’ve assigned numbers and names to all the accounts your company needs or may need in the future, your COA will look similar to this:

You can now use these accounts to track your transactions and create your company’s financial statements, including your income statement. Learn more about creating an income statement for your small business.